Expectedly, the pandemic has caused premium rates to grow even above the typical year-over-year increase of 5%. Self-insurance is a method employers can use to control these rising costs through careful plan design.

Self-Funded Strategies

Self-Funded Strategies Information

As health care costs continue to climb, employers are actively looking for impactful mitigation strategies. Expanding cost-sharing methods, such as offering high deductible health plans, has been one approach; yet, shifting costs onto employees might affect recruitment in a tight labor market. Instead, some employers are switching to self-insuring to reduce costs and improve service.

SELF-INSURED PLAN OVERVIEW

With a self-insured health plan, employers operate their own health plan as opposed to purchasing a fully insured plan from an insurance carrier. Essentially, fully insured and self-insured health plans can be identical in their plan designs (depending on setup); the main difference is how the plan is funded. Employers choose to self-insure in part to save the profit margin that an insurance company adds to its premium for a fully insured plan. However, self-insuring can expose the company to much larger risk in the event that more claims than expected must be paid. With a self-insured health plan:

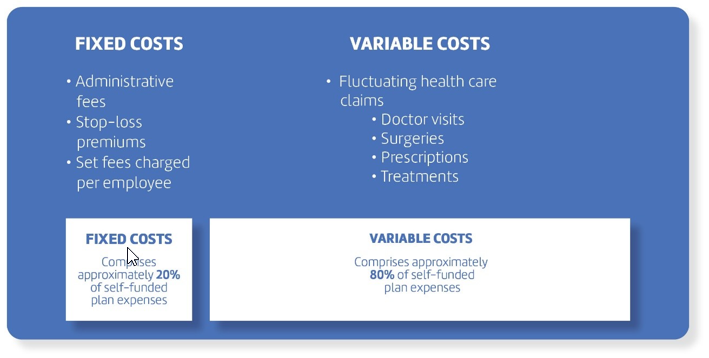

There are two main costs to consider

- Fixed Costs

- Variable costs

Some employers use stop-loss or excess-loss insurance to limit risk. This coverage reimburses the employer for claims that exceed a predetermined level. It can be purchased to cover catastrophic claims on one covered person (specific coverage) or to cover claims that significantly exceed the expected level for the group of covered persons (aggregate coverage).

Stop-loss is most closely comparable to a catastrophic coverage plan that indemnifies a plan sponsor from abnormal claim frequency and severity. Stop-loss claim reimbursements can be made for a variety of benefits, including medical, prescription drug, dental and others. Severe, high-dollar claims such as cancer, organ transplants and dialysis are considered “shock loss” claims, giving plans the most concern when assessing self-insuring. But, the protection afforded by a comprehensive stop-loss coverage shows its value in helping to financially manage these catastrophic events.

Self-Funded Strategies:

Attraction and Retention Advantages

In a tight labor market, offering the right perks can make all the difference. Self-insured health plans give employers more control over their offerings. For instance, they can set worker contribution levels and design plans to provide more benefits than a typical health plan. And, when health plans are designed with employees in mind, top performers are enticed to stay with a company longer.

Reduced Insurance Overhead Costs

Carriers assess risk charges and profit margins for insured policies (approximately 3%-5% annually), but self-insurance removes this charge.

Reduced State Premium Taxes

Self-insured programs, unlike insured policies, are not subject to state premium taxes, which typically amount to around 2-3% per year.

More Cost Control

When paired with stop-loss insurance, self-insured plans allow for a more accurate prediction of how much the employer may need to spend in a plan year. With this coverage, any costs over a certain amount are paid for by the carrier.

Avoidance of State-mandated Benefits

Although both fully insured and self-insured plans are governed by federal law (predominantly ERISA), self-insured plans are exempt from state insurance laws. State benefit mandates can add to the cost of insured employer benefit programs. For multistate employers, self-insuring can help create national consistency by elimination of the need for state-by-state compliance.

Employer Control, Generally

Employers who want to revise covered benefits and the levels of coverage are free from state regulations mandating coverage and the carrier negotiation typically required with changes in insured coverage. By self-insuring, employers are able to design their own customized health benefit packages.

Improved Cash Flow

Claims are paid as they become due; employers do not need to prepay for coverage. There is also a cash flow advantage in the year of adoption when “runout” claims are being covered by the prior insurance policy. Employers pay for claims rather than premiums and earn interest income on any unclaimed reserves.

Choice of Claim Administrator

An insured policy can be administered only by the insurance carrier. A self-insured plan can be administered by the company, an insurance company or independent TPA, which gives the employer greater choice and flexibility. When selecting a TPA, employers should consider whether the TPA efficiently handles claims; has contacts with stop-loss carriers, a strong reputation, cost management skills and negotiating clout; has medical expertise on staff; and provides excellent customer service and claims administration.

Greater Claims Projection

When a health plan is fully insured, a carrier owns the plan data. Self-insured plan data is completely owned by the employer, giving them access to more accurate claims analytics and health care utilization data that may otherwise be incomplete. Such data enables an employer to precisely budget for their annual health care spending